In response to the last column a reader wrote in on Twitter saying “shudder to think what would happen [to the stock market] if FIIs[foreign institutional investors] packed their bags and left.” Since the start of the financial crisis in September 2008 and up to October 2014, the FIIs have made net purchases (gross purchase minus gross sales of stocks) close to Rs 2.76 lakh crore in the Indian stock market. During the same period, the domestic institutional investors(DIIs) made net sales of Rs 95,219 crore.

The FIIs have continued to bring in money even during the course of this year. Between January and November 10, 2014, they had made net purchases of stocks worth Rs 65,751.25 crore. During the same period, the DIIs had made net sales of stocks worth Rs 30,136.32 crore.

Over and above this, the FIIs own around 26% of the BSE 100 stocks. Deepak Parekh in a recent speech estimated that after excluding promoter shareholding and the retail segment, which do not have too much liquidity, FIIs dominate close to 70% of the stock market.

What all these numbers clearly tell us is that the foreign investors run the Indian stock market. But that we had already established in the last column. In this column we will try and address the question as to what will happen if foreign investors packed their bags and left? The simple answer is that the stock market will fall and will fall big time. The foreign investors control 70% of the stock market and if they sell out, chances are there won’t be enough buyers in the market.

Nevertheless, the foreign investors also know this, so will they ever try getting out of the Indian stock market, lock, stock and barrel? This is where things get a little tricky.

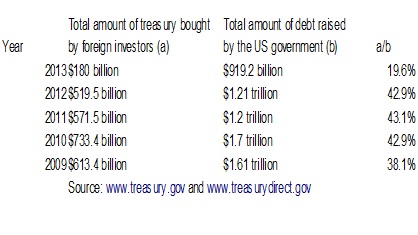

Let’s try and get deeper into this through a slightly similar situation in a different financial market. Over the years, the United States(US) government has spent much more than it has earned and has financed the difference through borrowing. As on November 7, 2014, the total borrowing of the United States government stood at $ 17.94 trillion dollars. The US government borrows this money by selling financial securities known as treasury bonds.

A little over $6 trillion of treasury bonds are held by foreign countries. Within this, China holds bonds worth $1.27 trillion and Japan holds bonds worth $1.23 trillion. Even though the difference in the total amount of treasury bonds held by China and Japan is not much, China is clearly the more important country in this equation.

Why is that the case? James Rickards explains this in great detail in Currency Wars—The Making of the Next Financial Crisis. The buying of treasury bonds by the Japanese is not as centralized as is the case with China, where the People’s Bank of China, the Chinese central bank, does the bulk of the buying. In the Japanese case the buying is spread among the Bank of Japan, which is the Japanese central bank, and other institutions like the big banks and pension funds.

The United States realizes the importance of China in the entire equation. Right till June 2011, China bought American treasury bonds through primary dealers, which were essentially big banks dealing directly with the Federal Reserve of the United States. But since then things have changed. The treasury department of the US (or what we call finance ministry in India) has given the People’s Bank of China, a direct computer link to its bond auction system.

Also, there is a great fear of what will happen if the Chinese ever decide to get out of US treasury bonds, lock, stock and barrel. It will lead to a contagion where many investors will try getting out of the treasury bonds at the same time, leading to a fall in their price.

A fall in price would mean that the returns on these bonds will go up, as the US government will continue paying the same interest on these bonds as it had in the past. Higher returns on the treasury bonds will mean that the interest rates on bank deposits and loans will also have to go up.

This can lead to a global financial crisis of the kind we saw breaking out in September 2008. Nevertheless, the question is will China wake up one fine day and start selling out of US government bonds? For a country like China, which holds treasury bonds worth $1.27 trillion, it does not make sense to wake up one day and start selling these bonds. This as explained earlier will lead to a fall in bond prices, which will hurt China as the value of its investment will go down. China has invested the foreign exchange that it earns through exports, in treasury bonds.

As on September 30, 2014, the Chinese foreign-exchange reserves stood at close to $3.89 trillion. Hence, nearly one third of Chinese foreign-exchange reserves are invested in US treasury bonds. Given this, it is highly unlikely that China will jeopardise the value of these foreign-exchange reserves by suddenly selling out of treasury bonds.

What China has done instead is that since November last year its investment in US treasury bonds has been limited to around $1.27 trillion. Also, some threats work best when they are not executed.

Hence, when it comes to the Chinese and their investment in treasury bonds, the situation is best expressed by the Hotel California song, sung by The Eagles: “You can check out any time you like, but you can never leave.”

Now let’s get back to the FIIs and their investment in the Indian stock market. Isn’t their situation similar to the Chinese investment in US treasury bonds? If they ever try to exit the Indian stock market lock, stock and barrel, it is worth remembering that they control nearly 70% of the market. When foreign investors decide to sell there won’t be enough buyers in the market. Hence, stock prices will fall big time, leading to foreign investors having to face further losses on the massive investments that they have made over the years.

Given this, are the Chinese in the US and foreign investors in India in a similar situation? Does the Hotel California song apply to foreign investors in India as well? Prima facie that seems to be the case. But there is one essential difference that we are ignoring here.

Nearly one third of Chinese foreign-exchange reserves are invested in US treasury bonds. Hence, China has a significant stake in the US treasury bond market. The same cannot be said about foreign investors in India’s stock market, at least when we consider them as a whole.

As Deepak Parekh said in a recent speech “India ranks among the top 10 global equity markets in terms of market cap. However, India accounts for just 2.4% of the global market capitalization of US $64 trillion.” Given this, in the global scheme of things for foreign investors, India does not really matter much.

Hence, if a sufficient number of them feel that they need to exit the Indian stock market, they will do that, even if it means that they have to face losses in the process. As mentioned earlier, in the global scheme of things, these losses won’t matter. Also, a lot of money brought into India by the FIIs has been due to the “easy money” policy run by the Federal Reserve of the United States and other Western central banks.

These central banks have printed money to maintain interest rates at low levels. The foreign investors have borrowed money at low interest rates and invested in the Indian stock market. Once these interest rates start to go up, it may no longer make sense for them to stay invested in India. Of course, it is very difficult to predict when will that happen.

Nevertheless, it is worth remembering what Steven Pinker writes in his new book The Sense of Style—The Thinking Person’s Guide to Writing in the 21st Century: “It’s hard to know the truth, that the world doesn’t just reveal itself to us, that we understand the world through our theories and constructs, which are not pictures but abstract propositions.”

And whatever I have written in today’s column is my abstract proposition. Hence, the question still remains: Will foreign investors ever sell out of the Indian stock market, lock, stock and barrel?